Following on from last week’s blog post (which you can find here) I will now go into more detail about the structural market problems facing Publishers and where an appreciation of the theory of complementary assets will improve understanding of these problems. As a reminder I made the diagram below that describes how the complementary assets model works in a market undergoing a transformation.

The most obvious thing to do to analyse the impact of programmatic is to compare the situation before the advent of programmatic and the situation now, i.e. what complementary assets were required before programmatic and what complementary assets are needed in the age of programmatic? The reason to ask about the situation immediately prior to the advent of programmatic advertising is to provide a benchmark for comparison and understand the direction of travel for the industry.

In the time before programmatic trading, the complementary assets required were principally ad servers and sales people. The ad servers were relatively freely available and generic, i.e. the market was relatively homogenous and ad server vendors competed on price. Provided that a site had either: a very focused audience or a very large audience, the advertising could be sold through the Publishers own efforts.

These days the complementary assets required to sell media programmatically are: audience data; technology platforms (e.g. SSPs and Ad Exchanges), and skilled staff. Audience data and technology platforms are relatively “tightly held” complementary assets because they are highly proprietary and in some cases completely out of the reach of Publishers. For example, we all know that a Publisher will never normally have access to advertiser or agency audience data. Agencies will typically cherry-pick impressions either in the open market or in a PMP and the Publisher will never truly understand the value of these impressions.

Many of the complementary assets used to sell digital media are tightly held by technology vendors

However, this is not specific niche case, but symptomatic of how the market is structured. In general audience and market data is collected by DSPs, SSPs, End-to-End Platforms, Ad Exchanges and Data Brokers on an ongoing basis. These enabling technology platforms ultimately work for either Publishers or Agencies (though sometimes directly with Advertisers). Nevertheless, they are also businesses in their own right and collect and exploit data for their own purposes. This means it is hard for a Publisher to restrict its audience data from reaching Data Brokers and the databases of Agencies. This loss of data through standard programmatic market operations is referred to in the industry as “Data Leakage”. In any case DSPs and Agencies tend to have a much wider view of the market than the Publisher, and in theory better market data sets from which to calculate prices because their systems work along the entire length of the value chain (I will talk about this in another blog post).

From a structural point-of-view, programmatic technology vendors link both buy-side and sell-side as well as enable the processing of audience and market data. While the buyer and seller technology trading layers only connect at the point of sale (e.g. SSP/DSP integration), the data layers of both buy-side and sell-side are active throughout the value chain (e.g. segmentation, targeting and reporting). This means that the entire value chain is effectively controlled by technology vendors either directly and obviously at the point of sale, or indirectly and less obviously in the way media is selected for purchase.

This data asymmetry is exacerbated by the fact that SSPs and Ad Exchanges do not reveal much of the market data in relation to the trading of the Publisher’s media. In addition, it is common practice for SSPs, Ad Exchanges and End-to-End Platforms to only present Publishers with a net payment figure for ad media after all intermediaries have taken their undisclosed commissions, thereby keeping Publishers in the dark as to the market value of their ad media. This means that Publishers have a far poorer understanding of their visitors than DSPs and Ad Exchanges, putting them at a further disadvantage in valuing or even selling their media.

Another area where Publishers, are at a data disadvantage is regarding the issue campaign management of programmatic campaigns. Even large Publisher who are in a good position to effectively manage programmatic campaigns using their own 1st party data, are strongly discouraged from doing so by agencies. Agencies want to do this themselves and use data they have bought from Data Brokers or in some cases client’s data.

It can also be argued that these complementary assets have gone from being generic (ad servers) to being much more specialised (audience data, market data, SSPs, DMPs, etc). For example, the complexity around data analysis and audience segmentation involves skilled staff and specialised technology. Indeed, building and sustaining the capability to analyse and segment audience data is an additional threshold barrier, since it can only be done with the relevant specialised complementary assets, i.e. skilled staff and a DMP. These represent significant additional scale threshold and ongoing costs to a Publisher, so could only be considered by larger Publishers. Therefore, programmatic has introduced not only specialised complementary assets, but also scale barriers!

Complementary assets? Major structural shift? What does this mean in reality?

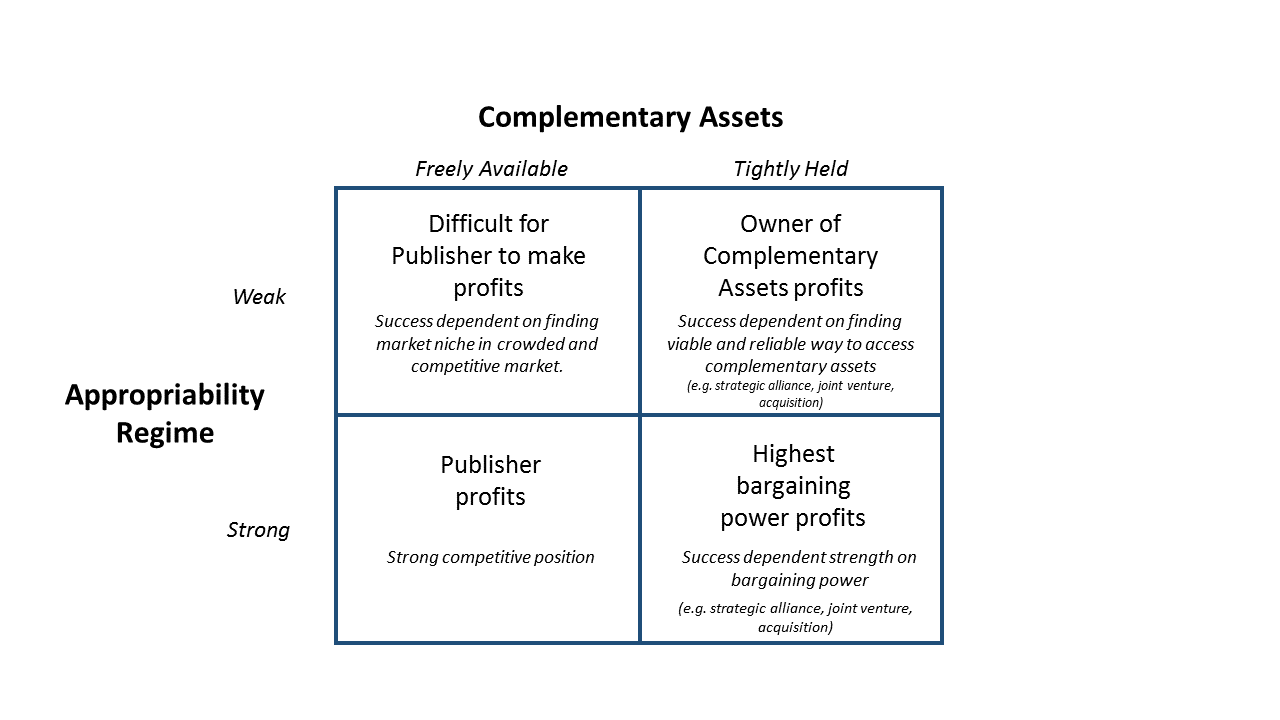

The point of the complementary assets model as explained in the previous post (here), is to predict/determine who will profit in the market that is undergoing transformation (in this case the digital media market being transformed with programmatic). The model can be used to predict who will benefit the Publisher or the holders of complementary assets (DSPs, SSPs, End-to-End Platforms, Ad Exchanges and Data Brokers). This model requires the analysis of two principal dimensions: appropriability regime and degree to which complementary assets are tightly held or freely available.

In the market for digital ad media, the appropriability regime is very weak, as there is nothing (or very little), to stop competitors or new entrants imitating a website or app, in theory, or in practice. Weak appropriability is very common and the market for digital media is no different.

As discussed above most complementary assets (SSP’s Exchanges, DMPs, Audience data and market data) are now more tightly held than previously. Complementary assets have gone from being freely available to tightly held, as shown below.

References: Teece (1986) Profiting from technological innovation: Implications for integration, collaboration, licensing and public policy. Research Policy. Elsevier B.V., 285-290 and 296-297

Enterprise Ad Server does not drop cookies, does not collect personal data from devices, and does not require consent to…

B2B publishers do not tend to use any monetisation ad technology because they sell all their ad inventory on a…

Today Rupert Graves from AdUnity spoke about data ethics and purposes for processing data at the EEMA. Rupert spoke about…

Today AdUnity announces the launch of the new privacy protected AdUnity Enterprise Ad Server for publishers (EAS). By default, the…

We have invested heavily in developing our privacy-by-design martech and ad-tech technology as required by GDPR (Articles 5, 11 and…

As part of our mission to get the advertising industry ready for GDPR AdUnity is pleased to announce that we…

{kind=link}

{kind=link}

{kind=link}