Does liquid soap have something to tell us about the programmatic media market?

When I first heard about complementary assets illustrated with the story of Robert Taylor and soap pumps, I realised there was a solid economic theory that explained many real world company failures and successes. I believe that the theory of complementary assets explains a lot of what we see in the programmatic display market today. This post is the first in a series of blog posts that explains how data and other complementary assets are transforming the market for digital media. This theory will also explain why a vast majority of Publishers are losing market power to ad tech companies and media agencies.

However, before I can start on this, I need to explain what complementary assets are! In addition, I will also need to provide some definitions for the things I will be referring to as complementary assets, in particular, different types of data. Therefore, this post is mainly about definitions.

Complementary Assets

Complementary assets have a specific meaning in economic theory, but they are generally thought of as a “thing that is required to successfully commercialise another product/service”. For example, cars are a complementary asset for car wash services (i.e. if people did not have cars there would be no car washes).

Complementary assets thinking can be found in the corporate strategy. An example would be Apple’s pursuit of its stand-alone ecosystem. All Apple products are designed to be highly complementary to each other, and less complementary to other brands of hardware. Once you have purchased one Apple product you are then incentivised to buy more as they work well together (in theory). The Apple example is a case of specialised complementary assets. There are also “generic” complementary assets. They are called “generic” because they do not have to be adapted to a particular use case. The Internet and more specifically broadband Internet is the huge generic complementary asset fueling digital media. However, when it was first marketed telecoms companies assumed they would provide all the services. They believed the Internet was a specialised complementary asset for them to provide new services. In fact, as we now know broadband Internet is a generic complementary asset and telecoms companies are generally terrible at providing other services.

There are many examples of the importance of complementary assets, however, the best example for me is the story of Robert Taylor. Robert Taylor was a US-based entrepreneur, who had the idea of selling liquid soap in dispensable pump containers. He had deep experience in the soap market so he recognised the huge potential market. Unfortunately, he couldn’t patent liquid soap or the pumps as both already existed on the market. Taylor knew that large soap companies would immediately copy his idea, launch competing products on a massive scale and put him out of business. His solution was to capture a specific complementary asset and significantly delay competitors from entering the market. Taylor ordered 100 million pump dispensers (two years worth of the entire national production) in order to stay ahead of the competition. After building a brand he successfully sold his business to Colgate-Palmolive for $61 million 1987. See here for more on this story.

It is clear that in the digital display market the advent of programmatic trading has brought whole new classes of complementary assets required by Publishers to sell their media. These complementary assets are: the technologies (e.g. SSPs, Ad Exchanges, DMPs and End-to-End Platforms); types of data (i.e. audience data and market data); and capabilities (e.g. ability to analyse and segment audiences).

Therefore, it is important to ask two key questions about these new complementary assets:

The implication is that if Publishers find that these new complementary assets are tightly controlled by other parties, then they have probably lost market power to the holders of these new complementary assets.

Definitions of Data

It is sometimes said that data has become the currency of the programmatic media market, i.e. no data no transaction! However, what do people really mean when they talk about data?

There are broadly two types of data that are vital for an understanding of how the programmatic media market works. Firstly, and most obviously there is audience data (i.e. data related to Internet users), and secondly, and hardly ever discussed is market data (i.e. data about transactions in the programmatic media market).

Audience Data

Data is collected about each visitor of a website or user of an app in order to calculate their propensity to buy different categories of goods and services. The browsing history, day, time, duration of visit, time on particular sites/pages, content of sites/pages, device type, configuration of device, frequency of browsing, geographic location, transaction history and many other data points are continuously collected by Data Brokers, e-commerce businesses and by Publishers. This data is put into a Database Management Platform (DMP) to analyse and simulate/model buying preferences, interests and intent to purchase. These preferences/interests/intents are collected so that groups of profiles can be aggregated into audience segments. Examples of interest segments would be “football fans”, “skiing enthusiasts” or “keen travellers”.

E-commerce businesses do this in order to use the data to sell their own goods and services, for example, an e-commerce site may use a Data Broker and its DMP to better segment its own customer base for retargeting purposes. Publishers will do this in order to better sell their audiences to Advertisers. This is particularly the case if the Publisher wants to negotiate a premium Automated Guaranteed deal, or if it was managing campaigns on behalf of advertisers (which large publishers often do) or a traditional IO.

Although audience data is generally understood to refer to people, it only refers to devices such as PCs and smart phones that people use. If two or more people use a device, such as a laptop, then no one-to-one relationship exists between device and person. This situation will make it very difficult, if not impossible, to create reliable profiles of the users of the device.

The main industry definitions of audience data relate to how it was collected and by extension who owns it. The main definitions are shown below:

Definitions of Audience Data

| X-Party Data | Whether data is first-party or second-party depends on perspective. First-party data is any information that is collected by an Advertiser or a Publisher through a direct relationship with an end-user or customer. As a result, there are two types: Advertiser first-party data and Publisher first-party data. |

| First-Party Data (Publisher) | Data a publisher can collect via its sites/apps. Sources of data include user behaviours, actions or interests; data in a Publisher subscription data; social data. Many inferences can be drawn from this data, such as intent to purchase and fit for a given audience profile. This data is free to Publisher but limited in scale and scope. |

| First-Party Data (Advertiser) | Data an Advertiser can collect, e.g. via social media or customer interactions. It is essentially the Advertiser’s customer records. Many inferences can be drawn from this data, such as intent to purchase and fit for a given audience profile. This data is free to Advertiser but limited in scale and scope. |

| Second-Party Data (Publisher) | This is another party’s first-party data. From the Publisher perspective, this data often belongs to the Advertiser, e.g. Advertiser customer data. |

| Second-Party Data (Advertiser) | This is another party’s first-party data. From the Advertiser perspective, this data most likely belongs to the Publisher, e.g. “interest data”. This data may or may not be included in the price of media, but in any case, it is limited in scale and scope. |

| Third-Party Data | Data collected by an entity that doesn’t have a direct relationship with end-user, Usually Data Brokers. It is collected at scale for the primary purpose of selling to advertisers for targeting individual Internet users. |

Market Data

Market data refers to data regarding the transactions in the programmatic media market. This includes: volumes of ad impressions on the market with respect to different sites, time periods, audience segments and location; prices of ad impressions with respect to different sites, time periods, audience segments and location; available media budgets; campaign goals; and actual performance of campaigns. Market data is collected by Agencies, DSPs and Data Brokers. No single business can collect all market data in order to analyse the entire market. Businesses tend to specialise in the type of data they collect or collect data with respect to their own campaigns.

Appendix: Complementary Assets for Geeks

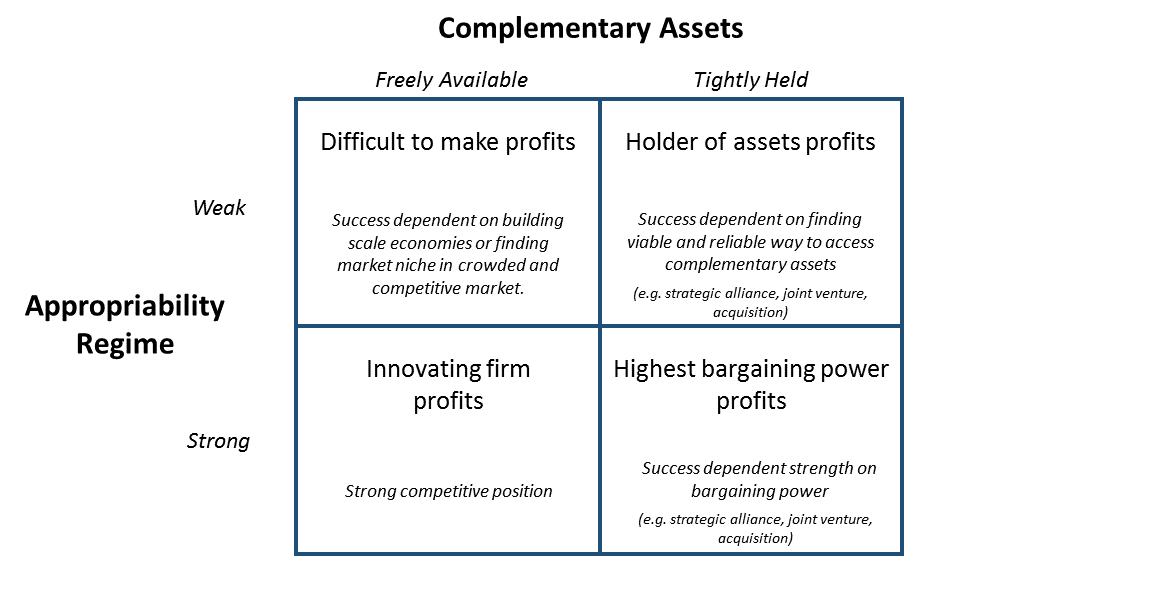

From an academic perspective, complementary assets were first defined by Teece (1986). His paper was intended to explain why, “innovating firms often fail to obtain significant economic returns from an innovation, while customers, imitators and other industry participants benefit.” (Teece, 1986, 285). In Teece’s paper, he considered two aspects of innovation, appropriability and complementary assets.

Appropriability is the ability of an innovating firm to exploit anmarket through legal mechanisms such as patents or copyright protection. An appropriability regime is weak if the firm can only use business strategy to prevent or limit imitation. Teece, 1986, 290)

Given the market and environmental variables of complementary assets and appropriability regime, Teece (1986) devised a model to indicate “the appropriate strategies for the innovators and predicts the outcomes to be expected for the various players.” (Teece, 1986, 296). As shown below with some adaptations from the Author.

References: Teece (1986) Profiting from technological innovation: Implications for integration, collaboration, licensing and public policy. Research Policy. Elsevier B.V., 285-290 and 296-297

Enterprise Ad Server does not drop cookies, does not collect personal data from devices, and does not require consent to…

B2B publishers do not tend to use any monetisation ad technology because they sell all their ad inventory on a…

Today Rupert Graves from AdUnity spoke about data ethics and purposes for processing data at the EEMA. Rupert spoke about…

Today AdUnity announces the launch of the new privacy protected AdUnity Enterprise Ad Server for publishers (EAS). By default, the…

We have invested heavily in developing our privacy-by-design martech and ad-tech technology as required by GDPR (Articles 5, 11 and…

As part of our mission to get the advertising industry ready for GDPR AdUnity is pleased to announce that we…

{kind=link}

{kind=link}